Why is the digital Inline XBRL format essential for structuring the IFRS annual and sustainability reports?

What is Inline XBRL? What are the IFRS and ESRS taxonomies about? Why are they so important in financial and sustainability reporting?

According to the requirements of the European Securities and Markets Authority (ESMA), the third-year running listed companies prepare their annual reports in the European Single Electronic Format (ESEF), and consolidated reports prepared in accordance with International Financial Reporting Standards (IFRS) are reported in iXBRL format with tagging.

In addition, the Corporate Sustainability Reporting Directive (CSRD) states that sustainability report for the year 2024, which must be submitted by public interest entities with 500 employees already in 2025, must be prepared in accordance with the European Sustainability Reporting Standards (ESRS) in the ESEF format and must be tagged in iXBRL.

Today new and modern financial and data analysis technologies are conquering the market every year. However, there are still global problems with financial data unification, traceability, data transparency, comparability of financial statements, and effective data analysis on a global scale.

While the business has been striving for automation, more and more new ERP systems and accounting programs are placed on the shoulders of financiers and accountants, which significantly complicates the reporting process. Especially in the aspects of collecting and analyzing large amounts of data. Despite the fact that XBRL was invented by a certified accountant in 1998, it is only now being actively used in financial and non-financial reporting in almost all countries around the world.

What is XBRL?

XBRL is an abbreviation of "eXtensible Business Reporting Language. In other words, XBRL is a unified XML-based data extension for business reporting that uses digital taxonomies to provide semantic elements for metadata.

What is Inline XBRL (iXBRL)?

While XBRL is only a machine-readable format, iXBRL (Inline XBRL) is both a human-readable and machine-readable format, as it is embedded in XHTML.

What is XBRL Taxonomy?

As defined by the European Securities and Markets Authority (ESMA), a taxonomy is an electronic dictionary that defines and links data elements and their relationships for reporting purposes. In other words, it is based on a scheme or structure corresponding to the relevant report's reporting regulation. The XBRL Taxonomy ensures efficient comparison of reports prepared in accordance with IFRS, even on a global scale.

As Examples could be mentioned:

- IFRS consolidated financial statement reporting in ESEF format, based on ESMA ESEF XBRL Taxonomy, which structure and granularity level corresponds to the International Financial Reporting Standards (IFRS);

- Sustainability report in iXBRL format, based on ESRS XBRL Taxonomy, which structure and granularity level corresponds to the European Sustainability Reporting Standards (ESRS);

It should be noted that several XBRL taxonomies, such as IFRS and ESRS XBRL taxonomies, may be applied simultaneously in one integrated annual report consisting of financial and sustainability reports.

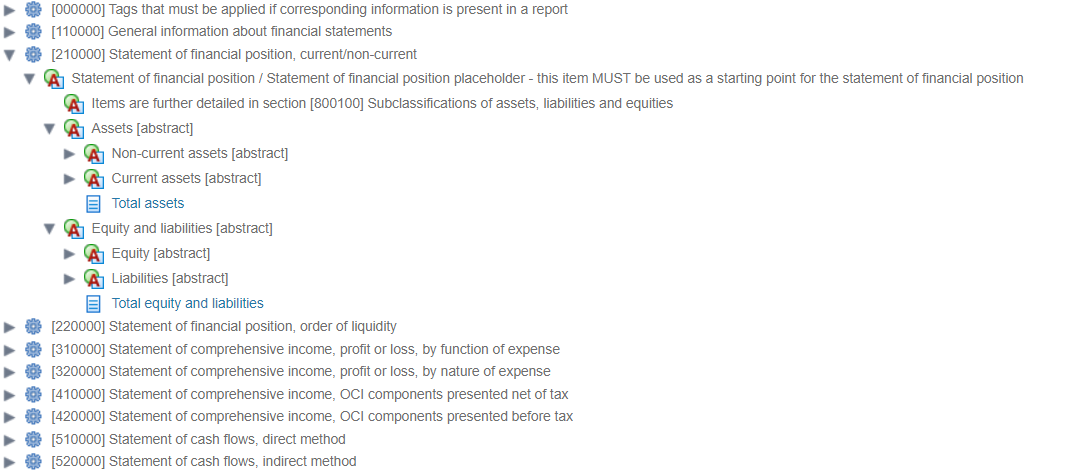

ESMA ESEF XBRL Taxonomy 2022, an example of a structured representation of the IFRS elements that make up the XBRL taxonomy:

XBRL reporting object

Any financial report is a logically structured collection of words and numbers that reflect a company's financial position and performance over a certain period.

The structure is the basis of any financial annual report, which is determined by a regulatory requirement, for example, IFRS, in the case of a sustainability report - ESRS, or by regulation of the national legislation of the relevant country. Although companies prepare financial annual reports according to the same legislation, following the same principles, the formats of these annual reports do not correspond to machine-readable ones. Therefore, makes it difficult for artificial intelligence analysis tools to structure and sequentially analyze that data. Why?

Let's take a look at the example:

Five different companies in Latvia, the United Kingdom, and Finland prepared their financial annual reports based on IFRS. The first table on the left contains the names of “Total Liabilities” as reported by the companies. Despite the fact that the nature of the values is the same, the names of the “Total Liabilities” item in the Financial statements for the three Latvian companies are different. On top of that, the “Total Liabilities” item is also presented in other languages for foreign companies. In addition, companies with the same reporting language may use different terminology for the same Financial statement items (see table with example above). There can also be differences in the presentation of:

- the dates,

- the decimals,

- the decimal separators (comma or point),

- the scale,

- the extension of the reported file.

That significantly complicates the collection, comparison, and analysis of the reported data by the analysts, or even makes it impossible.

In the example table on the right, an XBRL label (or tag) from the ESMA ESEF XBRL taxonomy with a single name: "ifrs-full:EquityAndLiabilities" is assigned to the “Total Liabilities”. By assigning XBRL tag, additional information or context is added to each tagged value, which specifies the format, decimals, currency, period, scale, and other required information of the reported value. This is the moment when data is transformed from unstructured to structured, which is excellently understood by XBRL-based analytical tools.

In the sense of iXBRL, structured data is a set of data where each reported element (numerical or textual value) is assigned with an XBRL taxonomy label (or tag), which itself contains all the information necessary for analysis: hierarchical placement in the IFRS taxonomy, the corresponding data type, period, currency, format, scale, etc.

Why financial and sustainability reporting is moving to iXBRL format?

The main idea is the unification of data on a global scale.

First of all, this format helps to transform data from unstructured to structured, where certain regulatory requirements / well-known reporting standards serve as the basis of the structure.

Secondly, the iXBRL format provides more accurate and efficient ways for financial and sustainability reporting analysis, which enables intsant quick and accurate analysis of a large set of data. In this context, it is important to know that the iXBRL data format is mostly used by systems with a built-in artificial intelligence engine. For example, using the XBRL-based analytical system, an investor can instantly calculate the "earning per share" for all European listed companies in all possible dimensions (by year, sector, geographical distribution, etc.).

Thirdly, XBRL taxonomies have been translated into more than 30 world languages, enabling an investor in Spain to get an analysis of the financial annual report of a Latvian company without additional translation efforts.

What are the main benefits of implementing iXBRL in financial and sustainability reporting?

From an investor's point of view, new investment opportunities appear as the range of companies available for analysis is rapidly increasing.

Applying the iXBRL format increases the efficiency of the company’s analysis and decision-making process, giving wider opportunities for market data insights. Until now, financial annual reports were reported mostly in PDF format – which is a non-machine-readable format. Shortly after the implementation of iXBRL, there is no longer a need to analyze each company's annual report separately. Annual reports are analyzed automatically with the XBRL-based analysis tool in seconds.

On the business side, it is a unique opportunity for obtaining external investments. Financial annual reports in iXBRL format will be available to a wider range of users. Besides, the language of the report will no longer matter as much. Geographical boundaries for attracting an investor or partner disappear. Also, in 2027, the European Single Access Point (ESAP) will be available, where the information of publicly reported financial and sustainability reports of European companies will be publicly available.

From the regulator's side, XBRL facilitates data collection and statistical reporting processes, improves the traceability and transparency of information reported in annual reports, and reduces the risks of fraud on a global scale.

Read also: IFRS 18 will be the first standard developed in cooperation with the digital team.

Want to know more about the iXBRL format for IFRS or sustainability reporting information, or to take a look at IFRS or ESRS digital taxonomy, email our Digital financial analyst, Svetlana Komarova, at s.komarova@orients.lv. Or, read more about the ESEF (iXBRL)-compliant digitalization services of the reporting at our website: https://www.orients.lv/en/expertise/esef-reporting/.